TIMIA’s Market Outlook Q1 2023

Published on

The recent fallout of SVB came as a blow to many in the tech sector, leaving those connected to the bank uncertain about the future. However, once the Feds stepped in, startup founders who rely on SVB for loans and financial operations could breathe a sigh of relief.

Now that the dust has settled, we’ve had time to reflect on what this incident means for the tech industry and the opportunities it presents. Here are some of my thoughts on the current events.

How did the SVB fallout affect TIMIA?

Little to no impact on TIMIA or our portfolio — As some of our portfolio companies were customers of SVB, we were quick to reach out and offer our support. The following days were chaotic for those founders as they navigated through information, assessing the impact on their business, opening secondary bank accounts, and ensuring payroll and payments were processed. Fortunately, the intervention of the Feds helped to calm things down. We’re happy to report that our portfolio companies have weathered the storm, and it’s business as usual for us.

How did the SVB fallout affect the tech ecosystem?

It will come out stronger — The tech community is known for being tight-knit and supportive. While it’s a competitive field, it’s also massively collaborative. Healthy competition is fostered by a diverse ecosystem that supports all stages and types of tech companies. Community members have created formal and informal networks where information and introductions flow freely.

The tech community’s success is due to the critical mass of all players, including startups at every stage, universities, incubators, accelerators, VCs, angel investors, venture debt providers, banks, partner channels, and more. SVB played an important role in this community, but the market will adapt and opportunities will arise for other fast-moving players to fill the gap left by its fallout.

What will happen in the future?

Banking regulations will tighten — While it’s too soon to say exactly how and when regulations will evolve, we believe it’s a positive step toward a more stable and secure banking system. As a Canadian-based company, we are familiar with tighter regulations than those in the USA, and we’ve seen firsthand the benefits of a stable and secure banking system. We’re optimistic that the right regulatory changes will be implemented to prevent similar incidents from occurring in the future.

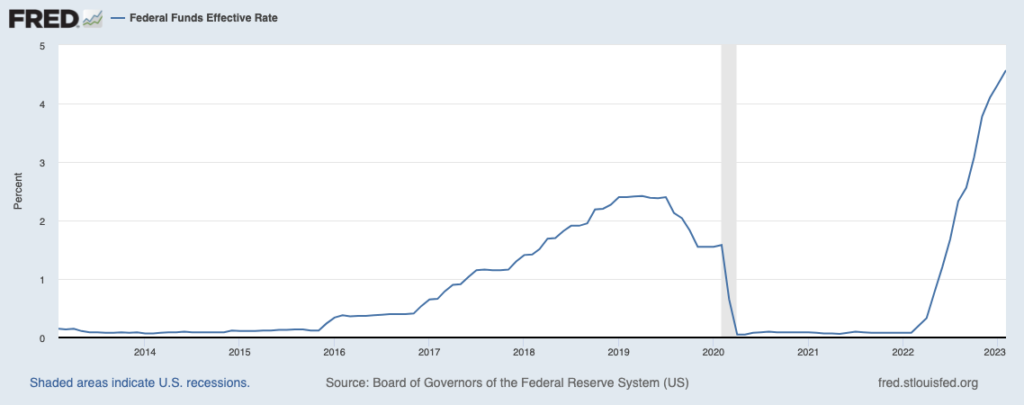

What will happen with interest rates?

Rates will hold relatively steady in the near term — Until inflation comes under control, rates will stay relatively steady; maybe up and down a bit. There has been significant discussion surrounding the recent interest rate hikes (including another small one this week) by the Feds, which many believe were raised too quickly and over too short a period of time.

The Feds are expected to work towards rectifying the situation, aiming to lessen the impact of interest rates on deposit management. This was a major issue with SVB, and its fallout has highlighted the importance of ensuring interest rate policies are implemented with caution and care. We are optimistic the Feds will take the necessary steps to promote financial stability and prevent similar incidents from occurring in the future. We expect rates to remain at current levels at least until Q1, 2024.

Source: Federal Funds Effective Rate

Will venture capitalists pick up the pace of investment?

Venture capital will continue to be tight —The second half of 2022 saw a slowdown in venture capital investment, as worries of an impending recession caused VCs to pull back and founders to reduce burn. Sales were also affected, as everyone waited to see what would happen.

Looking ahead, we expect venture capital to remain tight until the end of 2024. VCs will likely focus on supporting their existing portfolios while also seeking deals at lower valuations. However, we believe this presents opportunities for companies with strong financials and growth potential to secure investment and emerge stronger from the current economic climate.

Will tech sales stall?

Growth in tech sales is still shaky — During the second half of 2022, many startups experienced a softening in their sales due to talks of a possible recession. Buyers of software delayed their purchases or chose not to renew their contracts, resulting in a wait-and-see retrenchment across the industry.

However, in Q1 2023, we were seeing a pick-up in sales, indicating that the looming recession may be weaker than predicted. Our portfolio companies and applicants were showing positive growth, which makes the potential setback from the destabilization of the banking sector even more painful.

What is the outlook for startup survival?

Everyone will struggle to some degree — Pre-revenue startups will be more challenging than ever. While valuations have decreased, when you are at the $0-$5M stage, there isn’t a lot of room to negotiate. You either fund through family and friends, bootstrap through some alternate revenue stream while you build your tech or get angel investments.

Early stage startups with revenues of $500K to $2M or less and a high burn will be the most affected. They will have trouble surviving. It will be hard to get equity financing or debt financing. They will need to reduce burn and hunker down till valuations improve or find any type of exit.

Growth startups with revenues of $2M plus, good growth and strong financials will be able to get debt financing to accelerate their growth. Tech companies looking for a B or C round will want to wait until valuations improve in 12-18 months in order to avoid a down round.

For startups that did a big equity round in the last 24 months, some VCs are recommending they ‘throw in the towel’ — many raised too much, at valuations they will never grow to. The argument being that clean, well-planned exits now are better for everyone than messy ones in the future. If you are fortunate enough to be in the market to acquire (tech, team, clientbooks), you will be well positioned to get some deals.

What role will venture debt play?

Venture debt will thrive — As venture capital waits on the sidelines, venture debt is poised to fill the void. With the gap left in the market by SVB, all venture debt boats will rise. Banks are already cherry-picking SVB clients, and we expect deal flow to grow in both quality and size. We’re already seeing higher revenue companies with stronger risk profiles qualifying for larger facilities.

As a smaller player, TIMIA plans to support the ecosystem by growing our loan portfolio to help companies continue to grow. We’re confident our competitors will do the same, as the market has grown exponentially, and the need for reliable financing has become more pressing than ever. We wish them well, and we’re excited about the opportunities that lie ahead as the tech industry continues to innovate and adapt.

“In the uncertain banking climate, it is great to have someone who is willing to help support our mission.” — Timothy Holifield, CEO of SafePointe, a TIMIA portfolio company

Looking for non-dilutive capital?

TIMIA Capital works with B2B SaaS and software-enabled

companies between $2 – $20 million ARR.